Generally, just the project assets being financed. Personal guarantees are required from all 20% or more owners of the business.

SBA 504 Lending

PARTNER WITH US

SBA 504 Regular Loan Program

At the core of our values, we place great emphasis on delivering personalized service to our clients and partners. Our team consists of experienced professionals with specialized knowledge of SBA 504 Loans, ensuring successful financing and partnership at every step of the process.

Use of SBA 504 Funds

Acquire a building for the start-up, expansion, or relocation of your business.

Buy land and construct a brand new building that is perfect for your business operations.

Includes renovations and expansions of an existing property.

Finance major machinery and equipment purchases. This may include manufacturing equipment, medical devices, or other specialized equipment.

Additionally, both Building and Equipment financing may also include Furniture & Fixtures purchases for the business.

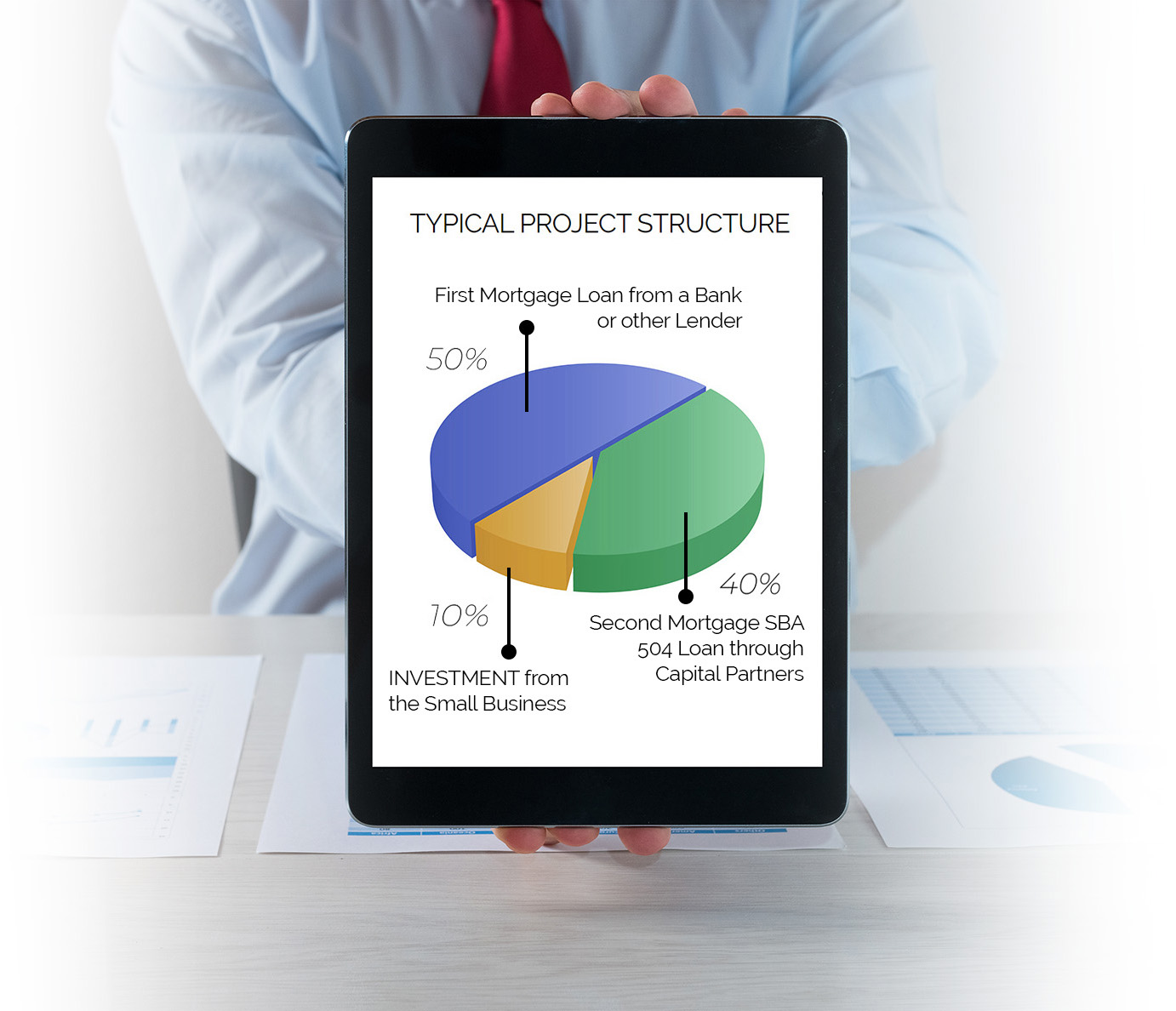

How is the 504 Loan Structured?

50%

LENDER 1ST MORTGAGE

- In some cases the 1st mortgage may be more than 50% to accommodate larger dollar projects.

- You negotiate the terms and fees with the bank, and whether it’s a fixed or variable rate.

- Lender’s Loan Term must be at least 10-years on 20/25 year project and 7-years on 10-year project.

40%

SBA 504 LOAN

- Payment Terms of 10, 20, and 25-Years Available – No Balloon Payment, No Renegotiation.

- Rate Fixed at 504 Loan Funding.

- Fees on the 504 loan currently total approximately 2.17% of the loan amount and 0.5% of the first mortgage loan amount.

- The 504 second mortgage cannot exceed $5 million, or $5.5 million for a Small Manufacturer or a Green Energy loan.

10%

BORROWER EQUITY

- Borrower typically provides a 10% down payment; however, loans for new businesses (less than 2-years) or for special-use facilities, such as hotels/gas stations, will require a 15% down payment OR 20% when the project is both new and special-use.

What Collateral is Pledged?

Prepayment Penalty on 504 Loan

Yes, you can pay off a 504 loan early; 504 loans with a 20/25-year term can be paid off with no penalty after the 10th year of the loan. Loans with a 10-year term can be paid off with no penalty after the 5th year of the loan.

504 loans with a 20 or 25-year term will have a re-purchase premium (RP) during the first ten years of the loan. This is a declining premium, 10% annually, that is calculated based on the year of the loan, remaining balance, and interest rate. For example, if a debenture is repurchased in year 5, the repurchase premium would be as follows: RP = Balance x (Note Rate x .50). Similarly, the 10-year loan has a repurchase premium for the first five years, and a declining penalty of 20% annually.